A recent Tribunal case considered the implications of claiming preferential duty rates when no certificate or statement of origin was present at the time of import.

Case Summary

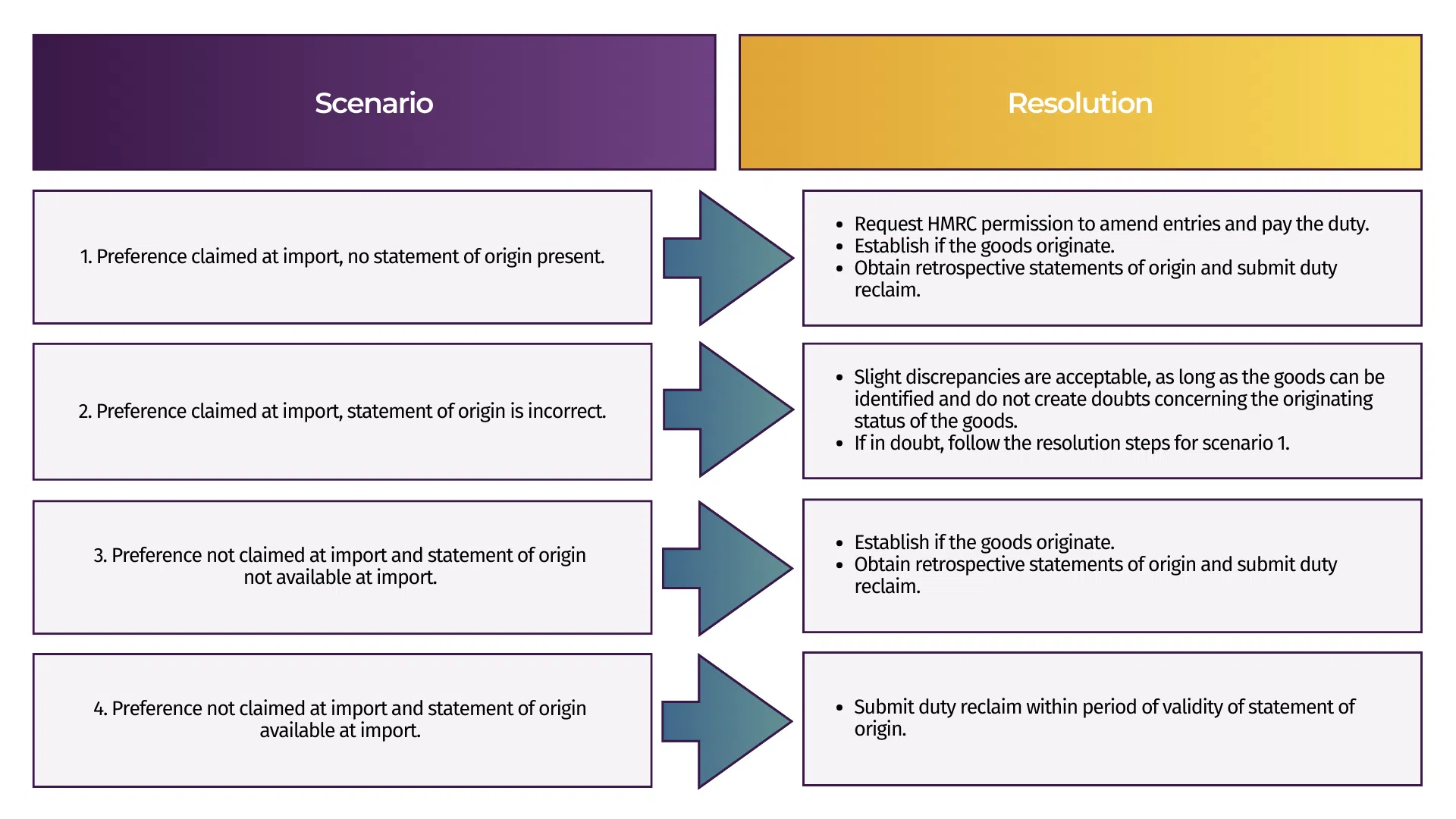

In a scenario familiar to many businesses, The importer’s customs agent claimed preference on imports from Italy, even though the invoices did not carry the required statement of origin. HMRC uncovered the issue during a routine post import audit when HMRC requested copies of invoices and statements of origin. They obtained and submitted to HMRC a retrospective statement of origin. However, HMRC rejected it and assessed the underpaid duty. The Tribunal ruled that the importers could not make a retrospective claim for the duty assessed.

Key Take-Aways

This is an important case for importers that take advantage of preferential duty rates through use of Free Trade Agreements:

- The importer is always responsible for the customs declaration, even though the agent may have made a mistake.

- The legislation requires a statement on origin to exist at the time the claim for preferential duty is made.

- The absence of a statement on origin at the time the claim for preferential duty is made cannot be retrospectively corrected by producing a retrospective statement on origin that was neither issued nor in existence at the time of the claim.

- An importer can only make a retrospective claim for preferential duty if:

-

- no claim for preferential duty was made on importation, and

- the customs duty was paid on importation, and

- the goods originate, and

- a retrospective statement of origin is available.

-

- If an error is made and preferential duty is incorrectly claimed on import, the importer has the option to amend the entries and repay the duty. Although not explicitly stated, the ruling implies that a retrospective reclaim may then be allowed if a correct, retrospective statement of origin is obtained.

- As the importer did not follow the procedure of withdrawing or amending the entries, they were not entitled to recover the duty. They were then time-barred from taking this action when the matter came to Tribunal.

Our Thoughts

This case highlights the fact that the importer is responsible for the customs declarations made on their behalf by customs agents. Control of import declarations is key, through instructions to customs agents and post-clearance checks.

If an error has occurred, it is important to amend any incorrect declarations as soon as possible and before HMRC indicate to the importer the intention to audit those entries, e.g. by providing the list of entries they require documentation for.

Once HMRC has approved the amendment of the entries are and the correct amount of duty is paid, the importer may submit a reclaim based on correct, retrospective origin evidence.

To ensure that preferential duty rates are correctly claimed:

- The importer must have dedicated staff with the necessary training and time to carry out post-clearance checks on the import declarations.

- The importer must work proactively with suppliers in preference giving countries to ensure the goods qualify for preference and are accompanied by the correct statement of origin.

- If there are any doubts on the accuracy of evidence of origin, the safe option is to pay the duty on import and reclaim it later (within two years of import for the Developed Countries Trading Scheme, three years for Free Trade Agreements).

We recommend all importers to undertake a review of their historical use of preferential duty rates, as HMRC are likely to increase their focus in this area since their success at Tribunal.

Barbourne Brook’s Customs Analytics software CAT360 quickly identifies potential at-risk transactions, ensuring swift and accurate resolution. Our expert consultants are ready to assist in addressing risks or errors, minimising the chance of additional customs duties.

Contact us today on +44 1905 914031 to learn more!

Talk To An Expert

Need help with customs compliance or looking to save on costs?

Share your contact details, and one of our experts will be in touch to assist!

Related Posts

Importers … Can You See What HMRC Sees? Unlocking Your Customs Data

Many businesses trust that their…