Minimising customs duties is crucial for improving margins, and while multiple planning options exist, choosing the right approach often comes down to weighing the advantages and disadvantages of each to achieve the same outcome.

Minimising customs duty costs is vital for businesses seeking a competitive advantage when sourcing from overseas as it improves gross margins. There are numerous tried-and-tested customs planning options (Barbourne Brook has over 160 in their internal knowledge database) applicable to different scenarios. But often, two different planning options could deliver the same outcome, each with advantages and disadvantages.

Lets Take a Closer Look

Let’s consider the following common business scenario:

- Materials sourced from a preference country (e.g. Mexico).

- Further worked in the UK.

- Then exported to the European Union.

- When asked, the supplier states they can provide the necessary supporting documentation to support a claim for preference.

What should the UK business do?

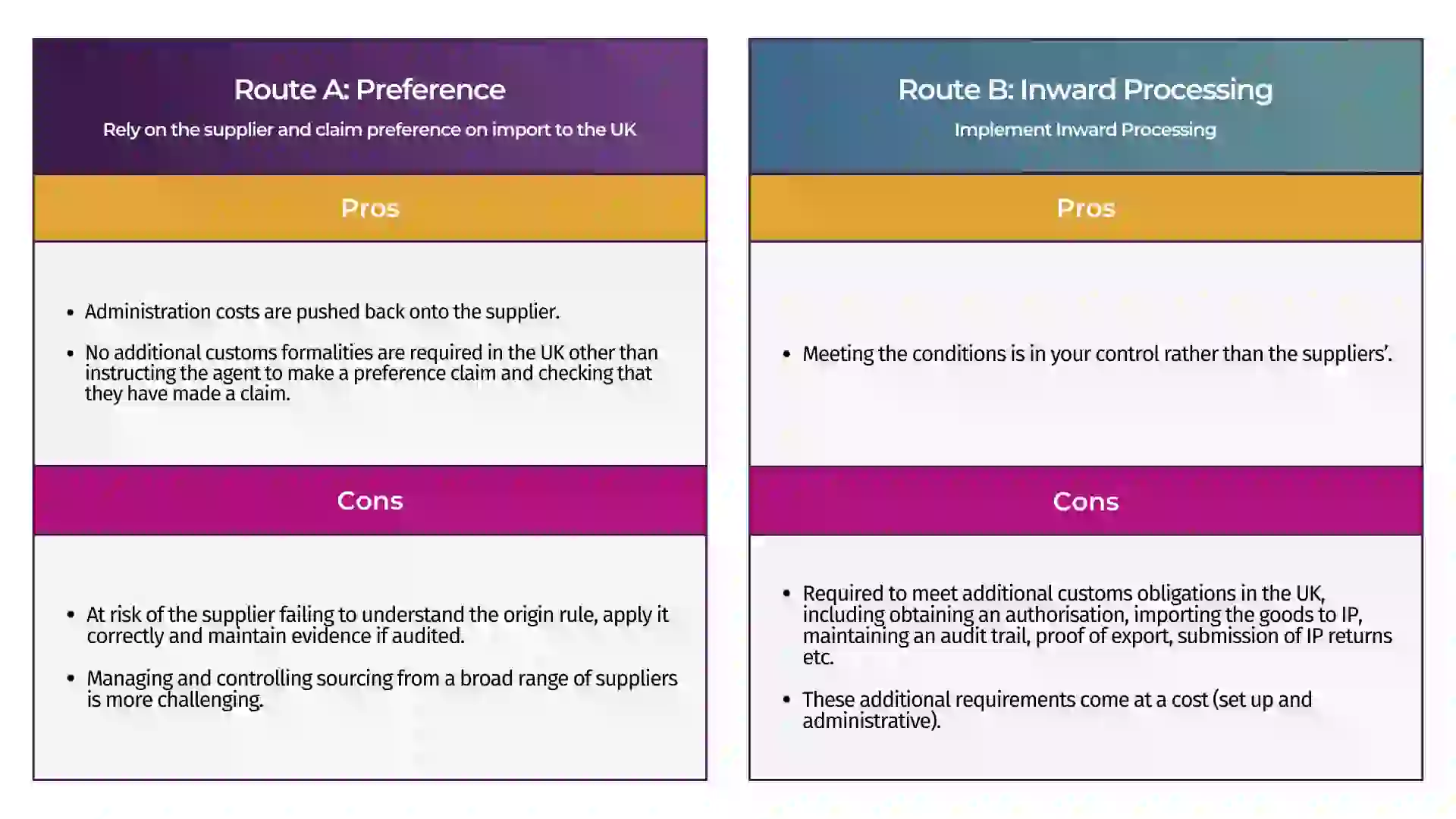

They either rely on the supplier and claim preference for import to the UK or implement Inward Processing.

If correctly applied, either option could mitigate customs duty costs in the UK. The decision is commercial, depending on the UK company’s risk appetite, the savings’ materiality and other possible nuances.

Factors to Consider

- The amount of customs duty savings. We recommend looking at this over three years, matching HMRC’s ability to audit and raise demands for non-compliance.

- Does the UK business export to an overseas market with whom we have an FTA? Some FTAs do not allow businesses to use IP and preference. Note that the European Union currently does allow this.

- What is the period between import and re-export? HMRC will limit the time granted to re-export the goods in line with the complexity of the work carried out.

- Does the UK business already operate IP? In this case, there is little additional cost associated with extending the relief to cover these goods.

- The relationship between the UK business and the supplier base, including transparency of operations, churn, the amount of control exercised and the number of suppliers.

In Conclusion

Choosing the most appropriate customs planning option depends on multiple factors. Critical to making this decision is identifying the underlying factors and assumptions.

Also, there are sometimes further options. For example, in the above scenario, the UK business could choose to use the FTA but take specific steps to mitigate the cons, including providing the origin rules to the suppliers, requesting evidence that the rules are met and seeking indemnity clauses in contracts to cover any customs duty demands, penalties and associated administrative costs.

Barbourne Brook works with clients to review all the options for reducing customs costs, reclaiming overpaid duty and reducing the risk of non-compliance. We also implement planning and provide ongoing support to ensure the conditions of any savings are met.

Adam Wood, CCO of Barbourne Brook, comments:

“When sourcing materials from a preference country, the choice between relying on supplier documentation or implementing Inward Processing hinges on commercial factors such as risk appetite, the materiality of savings, and other nuances. Both options, if applied correctly, can effectively mitigate customs duty costs.“

If this article raises important questions or cost-saving ideas for your business, reach out to Adam Wood today!

Related Posts

Protected: Product Recalls and Customs Duty: Hidden Costs, Missed Opportunities

In the food and beverage sector,…